"The scope of work for most matters is just too unpredictable to obtain a fixed fee."

This is a common misconception keeping many legal teams from realizing the tremendous benefits of using fixed fees in sourcing their outside counsel matters — cost predictability, cost control, and an outcomes-based relationship with their firms.

For example, we recently heard one PERSUIT client express skepticism over the utility of fixed fees in a complex litigation matter:

"There are hundreds of variables that determine the amount of work required from acting counsel. How could you possibly negotiate a fixed fee without a firm risking doing more work than was anticipated, or us (the Client) left paying unnecessary trial costs of a litigation matter that will likely resolve in a dispositive motion or early settlement?"

Here’s what we told them.

A good fixed fee isn’t actually “fixed” at all.

Sure, there is some risk sharing. But where there is risk, there is also reward.

Here’s our step-by-step approach to ensure fixed fee success for firms and clients alike.

Our Formula for Fixed Fee Success

A great fixed fee is one that is paired with a mechanism that allows for adjustments to the fee to be paid if there is a material change in the originally anticipated scope of work — or a “material deviation.”

So how then do you maintain cost predictability and control with fixed fees, while also allowing for these adjustments?

1. Identify the core cost-driving variables for the matter

In a litigation matter, these activities might consist primarily of certain activities to be performed by counsel, such as taking or defending witness depositions, reviewing documents, or conducting a trial over a period of days.

For a transactional matter, the key cost-driving variables might include specific elements of the transaction, such as the parties involved, size of the entities, or value of the deal.

We recommend limiting these cost-driving variables to those activities that are material to cost. Yes, outside counsel may spend their time involved in many different tasks, including phone consultations with the client, filing documents, and traveling to and from court. But in the context of a multi-million dollar litigation, these are not activities that should be material to cost.

Ultimately, we want to pay for outcomes, not effort.

Firms should naturally factor these minor variables in as activities required to perform the service and/or deliver the outcome.

2. Quantify the core cost-driving activities

These are your assumptions about the scope of work.

"Now hang on — I thought you said I don’t have to predict the trajectory of the matter?"

No one is expecting you to know exactly how many witnesses there will be or the number of documents that will need to be reviewed, but based on your experience with similar matter types and your read of the case, provide a reasonable assumed quantity. If you’re really not sure, make it up or ask an incumbent firm.

The goal here is to ensure your firms are providing fee proposals that are apples-to-apples so that you get a true sense of cost. You’re not asking your firms how much it will cost to represent you in this matter; you’re asking them how much it will cost for them to deliver an outcome, based on the available set of facts.

For example, in a straightforward M & A transaction, you can reasonably anticipate three rounds of negotiation of the final contract. While additional issues may arise as you work through due diligence and possibly require additional rounds of negotiation, your firms can still reasonably provide you with fee proposals based on the initial assumption that there will be three rounds of negotiation.

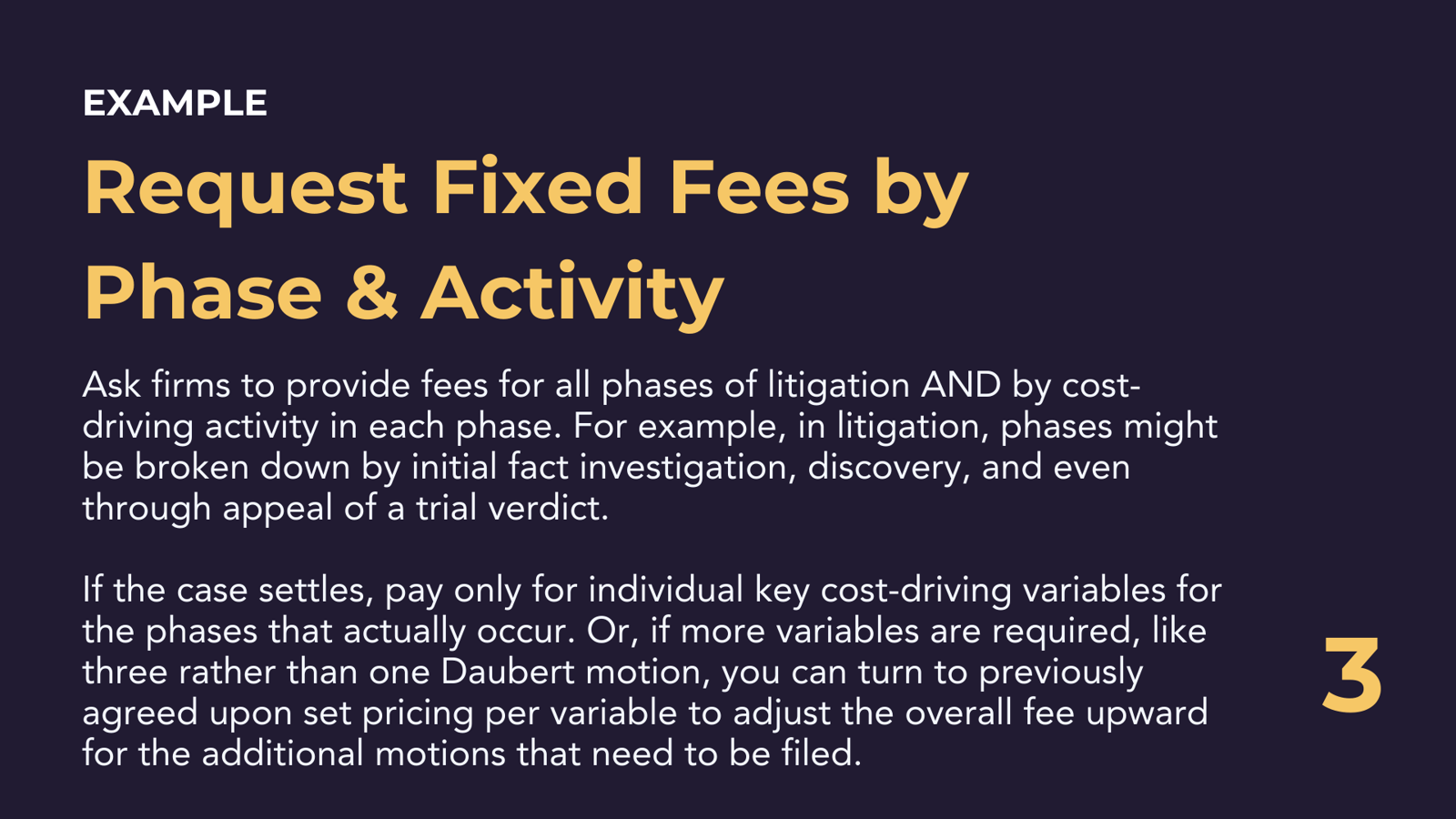

3. Ask your firms for fixed fees by phase and cost-drivers

When scoping and pricing the matter using the step above, your firms should be able to deliver you a Fixed Fee that is broken out by:

- Each phase or deliverable of the matter; and

- Core cost-driving variables within each phase.

This allows us to only pay for those phases as and when they occur and to deal with deviations in scope only with respect to those core cost-driving variables.

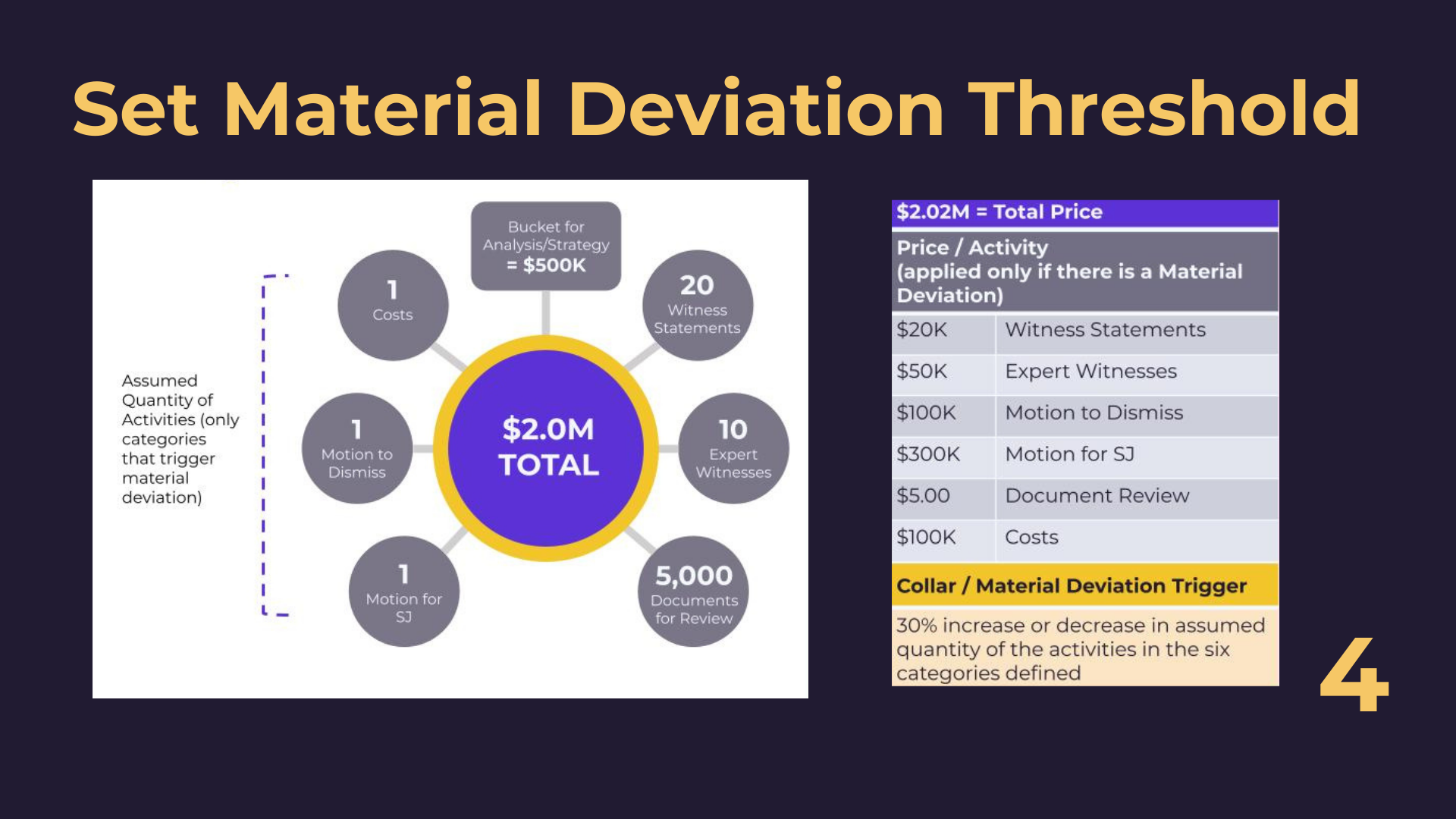

4. Set a threshold for Material Change in Scope (also often referred to as a Material Deviation)

In an effort to maintain cost predictability and control, we want to minimise the number of times a firm can come back to us and ask for a revision to the fixed fee. This means there is still an element of shared risk, but it comes with the benefit of cost containment.

We achieve this by limiting the flexibility in the fixed fee to only those changes in scope that we deem to be significant enough to warrant an increase or reduction in cost.

It is best practice to define a Material Change in Scope as a 30% increase or decrease in the Core Cost-Driving Variables.

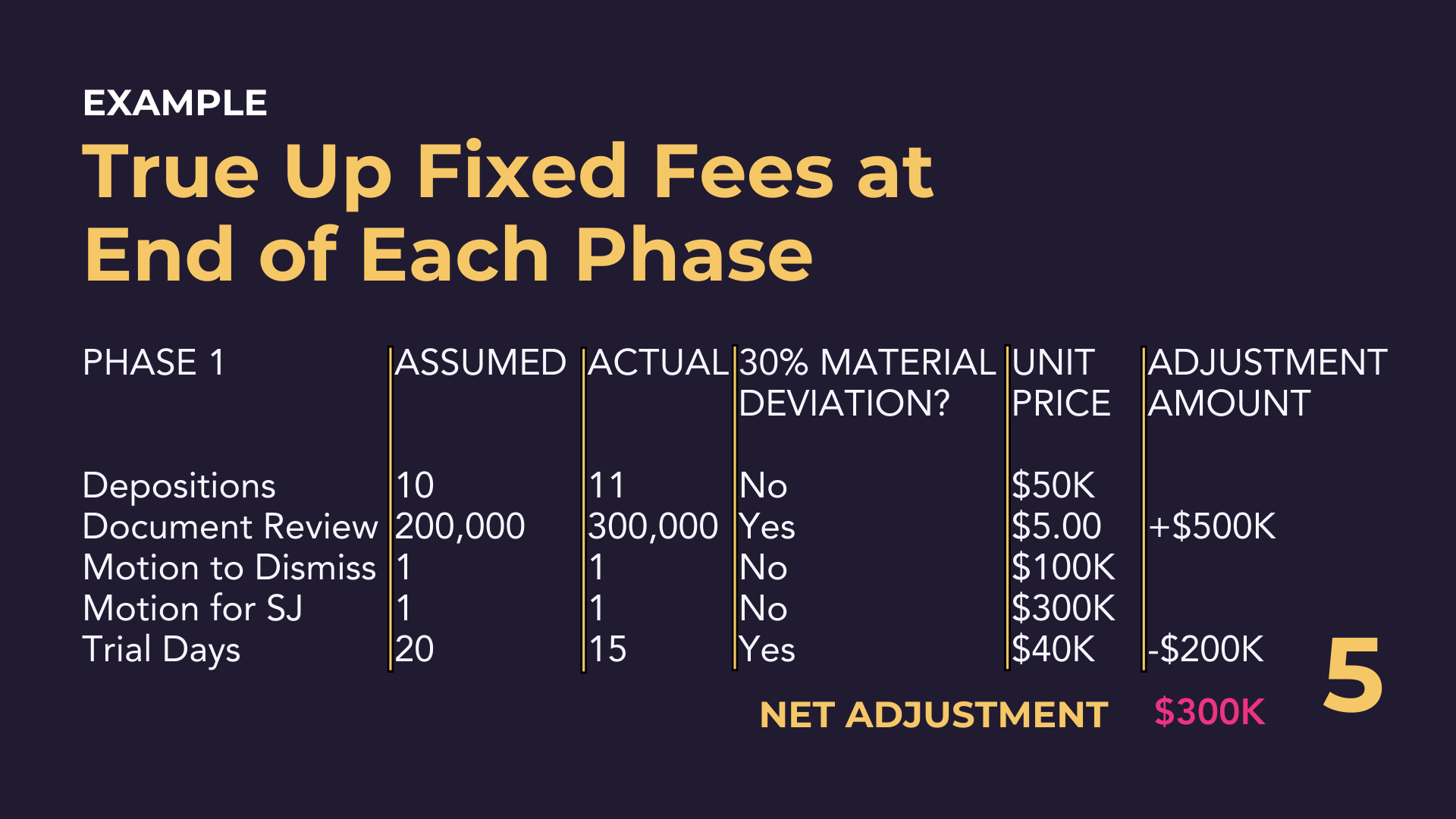

5. True up fixed fees at the completion of each phase and adjust for material deviations

At the completion of each phase, true up your fixed fee for that phase by comparing original assumptions to the actual assumptions to identify if there are any Material Changes in Scope.

Where there are, refer back to the pricing the firm provided for the Core Cost Driving Variables to determine how much to increase or decrease the price.

Make Fixed Fees a Win-Win

By using the above approach, you will:

- Achieve cost predictability — not because you’ll know exactly what you’ll spend on this matter, but because you know exactly how much it will cost for the firm to perform their services.

- Incentivize your firms to focus on the outcomes for each phase, rather than their billed time.

- Maintain control of costs so that if a phase blows up and significantly more work is required than anticipated, you aren’t at the mercy of the firms’ hourly rate and can have an open discussion with them about adjusting the fee, according to their initial fee proposal.

Not sure where to start?

PERSUIT has templatized this approach in its comprehensive library of RFP templates specific to matter type. Find out more here.